Skatteforpligtelser for PT PMA i Indonesien 2026

Hvis du netop har oprettet et PT PMA, eller hvis du har planer om at gøre det, er denne vejledning skrevet til dig. Uanset om du er en udenlandsk investor, direktør i et udenlandsk-ejet selskab eller en medarbejder i økonomiafdelingen, der prøver at finde ud af, hvad det indonesiske skattesystem egentlig forventer af dig, er du kommet til det rette sted.

Her er det korte svar, du har brug for lige nu: En PT PMA skal håndtere selskabsskat, en række månedlige kildeskatter, moms, hvis du er registreret som PKP (skattepligtig iværksætter), en årlig selvangivelse og i nogle tilfælde dokumentation for interne priser. Det er kernen i det.

Men detaljerne er vigtige, og hvis man tager fejl her, koster det rigtige penge. Skattereglerne i Indonesien ændres jævnligt, så du bør altid få din konkrete situation bekræftet hos en autoriseret skatterådgiver eller et registreret skatterådgivningsfirma.

Indholdsfortegnelse

Kort oversigt: Hvilke skatter skal en PT PMA betale?

| Forpligtelse | Hvornår det gælder | Indberetningshyppighed |

| Selskabsskat / PPh Badan | Virksomheden opnår et skattepligtigt overskud | Årligt |

| PPh 25 | Månedlige afdrag på selskabsskatten | Månedligt |

| PPh 29 | Årlig CIT-tilbetaling, når de løbende afdrag ikke dækker den endelige skatteforpligtelse | Årligt (inden indsendelse af SPT) |

| PPh 21 | Virksomheden har ansatte | Månedligt |

| PPh 23 | Betalinger til lokale leverandører for tjenesteydelser, husleje og royalties | Månedligt |

| PPh 26 | Betalinger til udenlandske modtagere | Månedligt |

| Moms / PPN | Virksomheden er registreret under navnet PKP | Månedligt |

| PBB (ejendoms- og bygningsskat) | Virksomheden ejer eller benytter skattepligtige grunde/bygninger | Årligt eller efter varsel |

| Bea Meterai (stempelafgift) | Visse officielle dokumenter og kontrakter | Pr. dokument |

| Dokumentation vedrørende interne priser | Transaktioner med nærtstående parter | En gang om året eller efter anmodning |

Bliver en PT PMA beskattet anderledes end en lokal PT?

De samme grundlæggende skatteforpligtelser som lokale virksomheder

Her er noget, som mange udenlandske investorer først indser, når de allerede står med papirarbejdet op til knæene: Et PT PMA er en fuldt ud indonesisk juridisk enhed. Det betyder, at det generelt er underlagt de samme indonesiske selskabsskatteregler som ethvert lokalt PT (aktieselskab). Indonesien anvender et selvangivelsessystem; din virksomhed er selv ansvarlig for at beregne, betale og indberette sine egne skatteforpligtelser for hver regnskabsperiode.

DJP, Generaldirektoratet for Skat, behandler dit udenlandsk ejede selskab på samme måde som et indenlandsk ejet selskab, hvad angår den grundlæggende rapporteringsstruktur. DJP kan dog stadig udstede et skattefastsættelsesbrev (SKPKB eller Surat Ketetapan Pajak Kurang Bayar) efter en skatterevision eller et opkrævningsbrev (Surat Tagihan Pajak / STP), hvis der mangler indberetninger, eller hvis der er betalt for lidt i skat.

Men der er yderligere udfordringer, som udenlandskejede virksomheder står over for

Princippet om “de samme regler” har dog sine begrænsninger. En PT PMA indebærer ofte komplikationer, som en rent lokal PT ikke omfatter:

- Udbytte til udenlandske aktionærer, udbetalinger til et moderselskab eller en udenlandsk investor udløser kildeskat i henhold til artikel 26

- Gebyrer for grænseoverskridende tjenester, hvis du betaler et udenlandsk firma for ledelses-, IT- eller tekniske tjenester, der medfører kildeskatteforpligtelser

- Anvendelse af skatteaftaler, hvis der findes en traktat mellem Indonesien og din aktionærs hjemland, kan du muligvis få en nedsat sats, men kun hvis du har de rette papirer (formular DGT)

- Intern prisfastsættelse, transaktioner mellem din PT PMA og nærtstående parter i udlandet skal foregå på markedsvilkår og dokumenteres

- Risiko for fast driftssted, hvis din udenlandske moderselskab er for involveret i driften, kan det blive betragtet som et BUT (fast driftssted) i Indonesien

Se det på denne måde: Skattegrundlaget er det samme, men der er bygget en ekstra etage ovenpå, der specifikt er beregnet til virksomheder med udenlandske forbindelser.

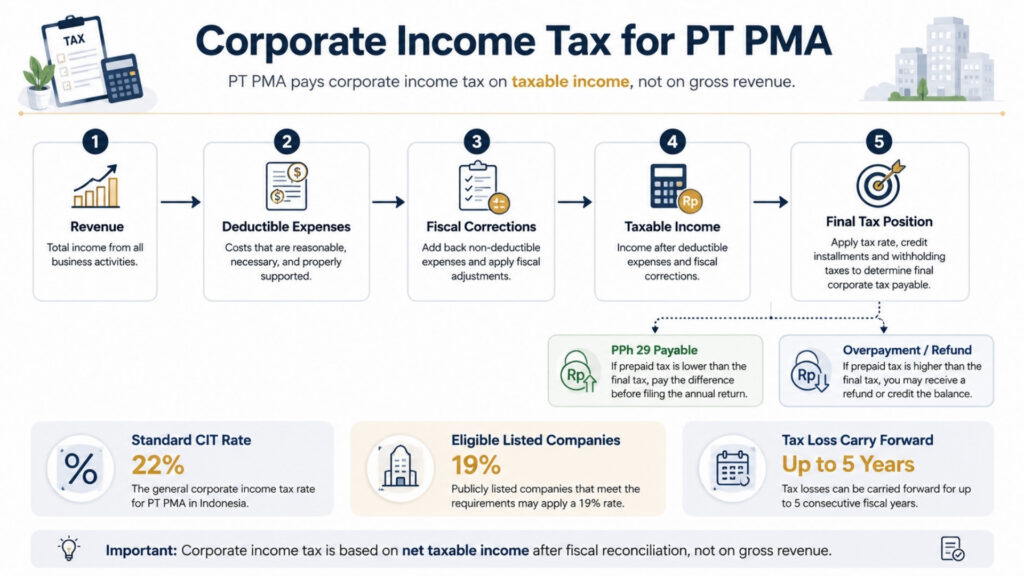

Selskabsskat for PT PMA

Den almindelige CIT-sats

Indonesiens standardskattesats for selskabsskat er 22% på den skattepligtige nettoindkomst, ikke på bruttoomsætningen, hvilket er en vigtig forskel. Man betaler kun selskabsskat af det beløb, der er tilbage, når man har fratrukket fradragsberettigede driftsudgifter fra sin indkomst.

Hvis din PT PMA er et børsnoteret selskab, der opfylder de minimale krav til børsnotering, kan du muligvis opnå en nedsættelse af skattesatsen i henhold til 3%, hvilket vil sænke din effektive selskabsskattesats til 19%.

Hvordan den skattepligtige indkomst rent faktisk beregnes

Det er her, mange udenlandske investorer snubler. Dit regnskabsmæssige overskud og dit skattemæssige overskud er ikke det samme.

Her er en enkel måde at se på det: Din revisor udarbejder regnskaber i overensstemmelse med de gældende regnskabsstandarder. Den indonesiske skattelovgivning følger ligeledes periodiseringsprincippet; indtægter indregnes, når de er optjent, og udgifter indregnes, når de er afholdt, uanset hvornår der rent faktisk sker en kontantbevægelse.

Men DJP har sine egne regler for, hvilke udgifter der er fradragsberettigede, og hvilke der ikke er. Denne forskel mellem regnskabsmæssig og skattemæssig behandling afklares gennem en skattemæssig afstemning (rekonsiliasi fiskal), som du skal foretage hvert år, før du kan indsende din årlige selvangivelse.

Typiske udgifter, der ikke er fradragsberettigede, omfatter repræsentationsudgifter uden behørig dokumentation, visse bøder og strafgebyrer samt personlige udgifter, der er blevet blandet ind i virksomhedens regnskaber – noget, der sker oftere, end man gerne vil indrømme. Skatteunderskud kan fremføres i op til fem år i henhold til de almindelige regler.

Skattefradrag for små virksomheder og den endelige skatteordning 0,5%

Her er to vigtige bemærkninger. For det første kan små virksomheder med en årlig omsætning på højst 50 milliarder IDR modtage en 50%-rabat på selskabsskatten, men kun på den del af den skattepligtige indkomst, der er knyttet til en omsætning på op til 4,8 milliarder IDR.

For det andet bør et PT PMA-selskab ikke gå ud fra, at det kan benytte den endelige indkomstskatteregeling 0,5%, blot fordi dets omsætning stadig ligger under 4,8 milliarder IDR. Nogle selskabsskattepligtige med en bruttoomsætning på op til 4,8 milliarder IDR kan falde ind under denne ordning, men berettigelsen afgøres fra sag til sag og er tidsbegrænset. Virksomhedens skattepligtige status, forretningsaktivitet, registreringsdato og valg af skattebehandling kan alle påvirke resultatet. Sørg altid for at få dette bekræftet hos en skatterådgiver, inden du anvender 0,5%-satsen i en skatteberegning.

Frist for indsendelse af den årlige selskabsskatteangivelse

Den årlige selskabsskatteangivelse, der kaldes Organets årlige SPT, skal indsendes senest fire måneder efter afslutningen af jeres regnskabsår. For virksomheder, der følger kalenderåret (januar til december), er fristen 30. april. For at indsende selvangivelsen skal du bruge dine regnskaber (samt reviderede regnskaber, hvor dette er lovpligtigt), din skatteafstemning og dokumentation for alle forudbetalte skatter, der er indbetalt i løbet af året.

Månedlige skatteforpligtelser for PT PMA

Det er her, det meste af det løbende arbejde ligger. Tænk på de månedlige skatteforpligtelser som et abonnement, man ikke kan opsige; de løber hver eneste måned, uanset om man har indtægter eller ej.

PPh 21 for ansatte

Hvis din PT PMA har ansatte – uanset om de er lokale eller udstationerede – er du forpligtet til hver måned at tilbageholde indkomstskat fra deres lønninger og indberette den. Dette er PPh 21. Det månedlige afkast for kildeskat for ansatte og udenlandske privatpersoner er SPT for indkomstskat (PPh) 21/26, der indsendes hver måned via Coretax.

Du skal bruge medarbejdernes NPWP-numre (eller NIK for dem, der ikke har et NPWP), lønoplysninger, der stemmer overens med dine BPJS-bidrag til social sikring, samt konsekvent indberetning via Coretax. I henhold til PMK-168/2023 anvendes der nu en effektiv sats (TER) til beregningen af den månedlige kildeskat i stedet for den gamle metode med skøn over nettoindkomsten.

PPh 23 for betaling af lokale tjenesteydelser

Hver gang din PT PMA betaler en lokal leverandør for tjenesteydelser, royalties eller leje af aktiver, der ikke er jord eller bygninger, såsom udstyr eller køretøjer, kan det være nødvendigt at tilbageholde PPh 23 fra betalingen. Leje af jord og bygninger behandles normalt separat i henhold til artikel 4, stk. 2, i den endelige indkomstskattelov, så du bør ikke medtage kontorleje i PPh 23 uden først at kontrollere skattegenstanden.

Kildeskatten i henhold til PPh 23 for betaling for lokale tjenesteydelser sammenlægges med andre kildeskatter i SPT Masa Unifikasi, den samlede månedlige kildeskatteangivelse, der indsendes via Coretax. Tjek din leverandørs skattestatus; nogle er fritaget, mens andre er underlagt andre satser. Manglende overholdelse af denne forpligtelse er en af de mest almindelige mangler i overholdelsen hos nye PT PMA’er.

Månedlige afdrag på selskabsskat (PPh 25)

Hvis din samlede forudbetalte skat er lavere end den endelige årlige selskabsskat, der skal betales, behandles det resterende underskud normalt som PPh 29, dvs. underbetalt årlig selskabsskat. Dette beløb skal betales, inden den årlige selskabsskatteangivelse indsendes. Derfor bør de månedlige PPh 25-afdrag, fradrag for kildeskat og den regnskabsmæssige afstemning ved årets afslutning kontrolleres samlet, inden indsendelsen.

Omvendt gælder det, at hvis dine PPh 25-afdrag overstiger din faktiske årlige skatteforpligtelse, vil du stå med en overbetaling på din selskabsskatteangivelse. Denne overbetaling kan modregnes i andre skatteforpligtelser via en pemindahbukuan (skatteoverførsel) eller kræves tilbagebetalt via en formel anmodning om skattefradrag til DJP. Begge fremgangsmåder kræver dokumentation, så sørg for at holde styr på dine betalingsoplysninger og afdragsberegninger gennem hele året.

PPh 26 for betalinger til udenlandske modtagere

Det er her, at overholdelsen af PT PMA-reglerne bliver mere kompliceret end for lokale virksomheder. Når din virksomhed udbetaler udbytte til en udenlandsk aktionær, renter på et lån fra en udenlandsk långiver, royalties til en udenlandsk varemærkeindehaver eller administrationshonorarer til et moderselskab, skal du tilbageholde PPh 26 til en standardatsats på 20%.

Men – og det er vigtigt – hvis der findes en dobbeltbeskatningsaftale (DTA) mellem Indonesien og modtagerens land, kan du muligvis være berettiget til en nedsat aftalesats. Du kan dog ikke selv anvende den lavere sats.

For passiv indkomst såsom udbytte, renter og royalties skal den udenlandske modtager være den faktiske ejer af den pågældende indkomst og skal fremlægge et bekræftet bopælsbevis (Certificate of Domicile, CoD), der indsendes som formular DGT til DJP. Uden et gyldigt CoD/formular DGT, der er godkendt af DJP, gælder standardsatsen for 20% uden undtagelser. Begrebet faktisk ejerskab er afgørende: hvis den udenlandske part er en mellemhånd eller en holdingstruktur snarere end den reelle økonomiske ejer, kan fordelen ved dobbeltbeskatningsaftalen nægtes, selvom formular DGT er indsendt.

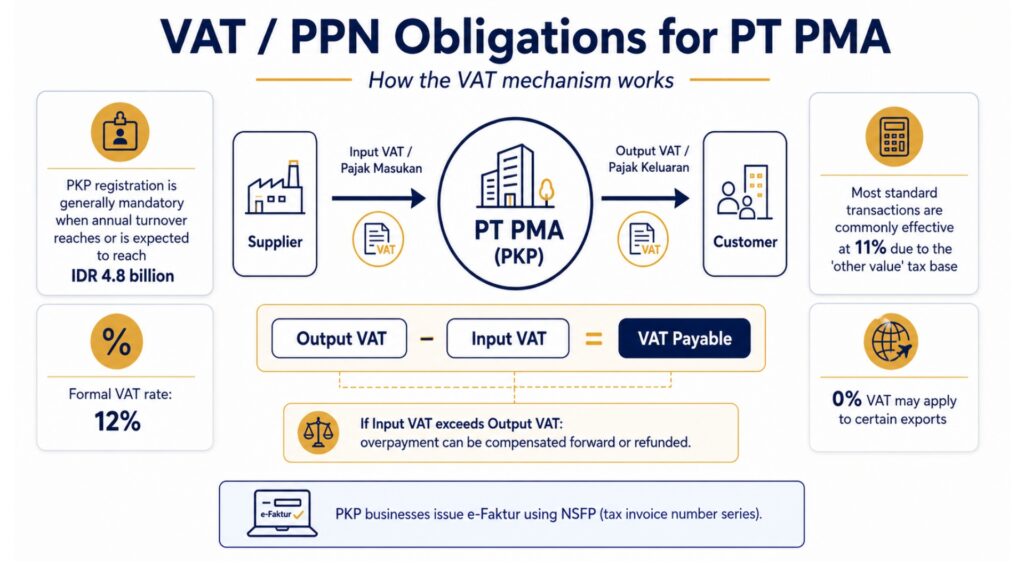

Moms-/PPN-forpligtelser for PT PMA

Hvornår skal en PT PMA registrere sig som PKP?

Når din PT PMA’s årlige omsætning når eller forventes at nå op på 4,8 milliarder IDR, skal du registrere dig som PKP (Pengusaha Kena Pajak), altså en skattepligtig virksomhed. Efter registreringen skal du opkræve moms på dit salg og kan få refunderet den moms, du har betalt på indkøb til virksomheden. Virksomheder i opstartsfasen kan også registrere sig frivilligt, før de når denne tærskel, hvis det er forretningsmæssigt fornuftigt.

Den nuværende momssats i Indonesien

Det er her, selv erfarne finansfolk kan blive forvirrede. Indonesiens Den officielle momssats er 12%. Men de fleste varer og tjenesteydelser beskattes stadig reelt med 11% på grund af en mekanisme, der kaldes DPP Andre værdier (andet skattegrundlag), et fiktivt skattegrundlag, der finder anvendelse på de fleste standardtransaktioner i stedet for den fulde transaktionsværdi. Den effektive sats på 12% gælder kun for visse luksusvarer. Eksport af varer og visse tjenesteydelser er fritaget for moms. Når du opstiller økonomiske modeller eller fastsætter priser på dine tjenesteydelser, skal du bruge 11% som udgangspunkt for de fleste standard B2B-transaktioner, men du bør altid få bekræftet dette hos din skatterådgiver for din specifikke virksomhedstype.

Momsfakturaer, indgående moms og almindelige fejl

Når du er registreret som PKP, skal du udstede skattefakturaer, kaldet e-Faktur, for hvert afgiftspligtigt salg. Disse skal udstedes via DJP’s e-Faktur-system ved hjælp af et NSFP (Nomor Seri Faktur Pajak, dvs. skattefakturanummer-serienummer), der tildeles af DJP. Pajak Keluaran (udgående moms), det beløb, du opkræver fra kunderne, minus Pajak Masukan (indgående moms), det beløb, du har betalt til dine PKP-leverandører, svarer til det beløb, du skal indbetale til staten hver måned.

Hvis indgående moms overstiger udgående moms i en given periode, har du en momsoverskudssaldo. Dette overskud kan overføres til den næste periode eller kræves tilbagebetalt via en formel ansøgning om momstilbagebetaling, hvilket, hvis den godkendes, medfører, at DJP udsteder en SKPLB (Surat Ketetapan Pajak Lebih Bayar), den officielle afgørelse om for meget betalt skat, der giver hjemmel til tilbagebetalingen.

Den mest alvorlige momsfejl? At overskride fristen for udstedelse af fakturaer. Indgående momsfradrag kan afvises, hvis fakturaen ikke er udstedt rettidigt eller ikke opfylder de tekniske krav. Et enkelt manglende felt i en e-Faktur kan betyde, at et fradrag på flere millioner rupiah afvises.

Andre skatter og overholdelsesforhold

Artikel 4, stk. 2: Endelig indkomstskat omfatter visse transaktioner, der beskattes endeligt, lejeindtægter fra jord og bygninger, bygge- og anlægsydelser samt nogle få andre poster. Satserne varierer alt efter kategori, og disse skatter er endelige, hvilket betyder, at du ikke kan trække basisindkomsten fra igen i din årsopgørelse.

PBB (ejendoms- og bygningsskat) opkræves nu som en regional skat i henhold til PBB-P2-reglerne med en maksimalsats på 0,5%, afhængigt af de regionale myndigheders bestemmelser. Den skattepligtige værdi baseres på NJOP (Nilai Jual Objek Pajak, dvs. den fastsatte salgsværdi). Det er værd at bemærke, at PBB-sektorregler gælder for visse brancher, herunder minedrift, olie- og gasindustrien, plantagedrift og skovbrug, som er underlagt særskilte PBB-bestemmelser fra centralregeringen i stedet for den regionale PBB-P2-ramme.

Hvis din PT PMA driver virksomhed inden for en af disse sektorer, adskiller de gældende PBB-regler, -satser og -indberetningskanaler sig fra den almindelige regionale skatteprocedure. Hvis din PT PMA overdrager jord- eller bygningsrettigheder, kan BPHTB (skat på overdragelse af jord- og bygningsrettigheder) også finde anvendelse med en maksimalsats på 5% af transaktionsværdien, der overstiger en bestemt tærskel.

Bea Meterai (stempelafgift) et beløb på 10.000 IDR gælder for kontrakter, aftaler og visse officielle dokumenter, der overstiger de angivne værdier. Det er let at glemme, men overraskende vigtigt i forbindelse med revisioner og juridiske tvister.

Lokale/regionale skatter (PBJT) I visse brancher kan hoteller, restauranter, underholdningssteder og lokale servicevirksomheder være forpligtet til at betale yderligere skatter til regionale myndigheder i henhold til loven om regionale skatter og afgifter. Dette er uafhængigt af de nationale skatteforpligtelser og kan komme som en overraskelse for PT-PMA’er med fokus på hotel- og restaurationsbranchen.

PPh 22, importmoms og toldafgifter

Hvis din PT PMA importerer varer til Indonesien, omfatter skatteforpligtelserne mere end blot selskabsskat og moms. Importtransaktioner kan omfatte importtold (Bea Masuk), importmoms (PPN impor), PPnBM (salgsafgift på luksusvarer) på visse luksusvarer samt indkomstskat i henhold til artikel 22 (PPh 22). Disse beløb afregnes normalt i forbindelse med toldbehandlingen, men de har stadig indflydelse på jeres skatteregnskab og den årlige skatteafstemning.

Dette er især vigtigt for PT-PMA’er inden for handel, produktion, byggeri, hotel- og restaurationsbranchen samt detailhandlen. Opbevar tolddokumenter, importangivelser, skattebetalingskvitteringer (fakturakoder), handelsfakturaer fra udenlandske leverandører samt samlede leverandørkontrakter. En handelsfaktura er det primære dokument, som toldmyndighederne bruger til at fastsætte den toldpligtige værdi, og din revisor vil også have brug for den til at afstemme importomkostninger, indgående moms (Pajak Masukan), lagerværdi og forudbetalt indkomstskat ved årets afslutning. Manglende eller uoverensstemmende handelsfakturaer kan skabe uoverensstemmelser mellem toldmyndighedernes registre og skatteangivelserne, hvilket ofte udløser en skatterevision.

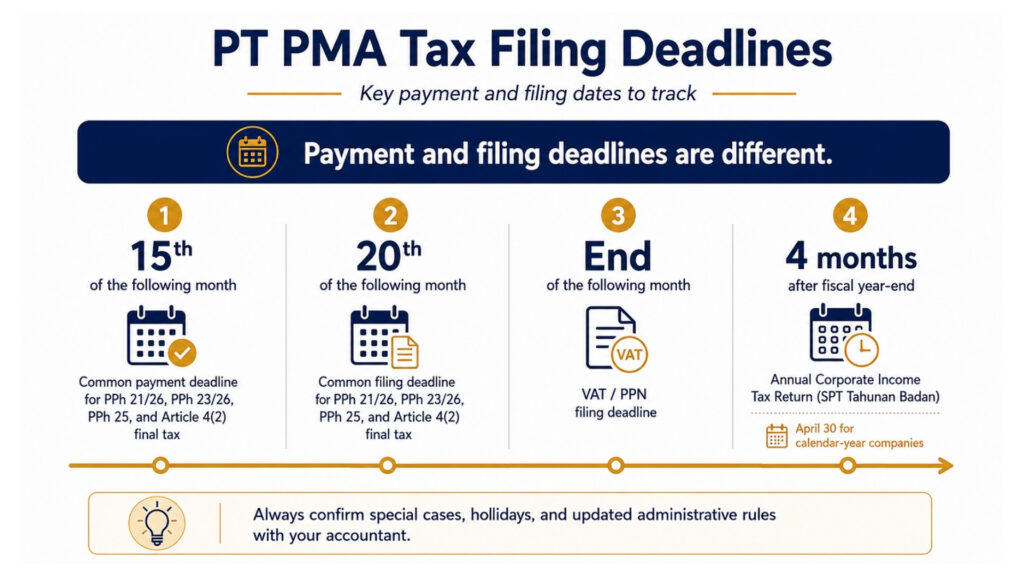

Frister for indgivelse af selvangivelser for PT PMA-virksomheder

| Selvangivelse | Indsendelsesfrist |

| Årlig selskabsskatteangivelse (SPT Tahunan Badan) | 4 måneder efter afslutningen af skatteåret (30. april for virksomheder, der følger kalenderåret) |

| PPh 21 / 26 (lønmodtager / kildeskat for udlændinge) | den 20. i den følgende måned |

| PPh 23 / 26 (tjenesteydelser / kildeskat for udlændinge) | den 20. i den følgende måned |

| PPh 25 (månedlig rate af selskabsskat) | den 20. i den følgende måned |

| Artikel 4, stk. 2: Endelig indkomstskat | den 20. i den følgende måned |

| Moms / PPnBM | Slutningen af den følgende måned |

Fristerne for betaling og indsendelse er ikke de samme; dette er en praktisk uoverensstemmelse, som mange PT PMA’er snubler over. Her følger en mere overskuelig oversigt:

| Skattetype | Betalingsfrist | Indsendelsesfrist |

| PPh 21 / 26 | Som regel senest den 15. i den følgende måned | Senest den 20. i den følgende måned |

| PPh 23 / 26 | Som regel senest den 15. i den følgende måned | Senest den 20. i den følgende måned |

| PPh 25 | Som regel senest den 15. i den følgende måned | Senest den 20. i den følgende måned |

| Artikel 4, stk. 2: Endelig skat | Som regel senest den 15. i den følgende måned | Senest den 20. i den følgende måned |

| Moms / PPN | Inden indsendelse af momsangivelsen | Slutningen af den følgende måned |

| Årlig selskabsskat / Årlig selskabsskat for selskaber | Inden indsendelse af årsopgørelsen | 4 måneder efter regnskabsårets afslutning |

Forsinket betaling medfører rentetillæg, der beregnes på grundlag af den gældende månedlige rentesats fra Finansministeriet (MoF) plus et tillæg, i op til 24 måneder. Forsinket indsendelse medfører også separate administrative bøder: 100.000 IDR for de fleste månedlige selvangivelser, 500.000 IDR for en forsinket momsangivelse og 1.000.000 IDR for en forsinket årlig selskabsskatteangivelse. Tjek de aktuelle satser hos din revisor, da Finansministeriets rentesats fastsættes med jævne mellemrum.

En praktisk bemærkning om, hvordan betalinger foregår: Skattebetalinger i Indonesien foregår via en bankopfattelse, en af regeringen udpeget bank eller betalingskanal, der er bemyndiget til at modtage skatteindbetalinger på vegne af DJP.

Betalinger foretages ved at generere en faktureringskode (Kode Billing) i Coretax og afregne den via en bank persepsi eller en godkendt e-betalingskanal. Hvis dit PT PMA har et overskud på en bestemt skattetype, som du ønsker at modregne i en forpligtelse vedrørende en anden skattetype, sker dette via overførsel (en skattebogføringsmæssig overførsel), en formel anmodning til DJP om at overføre kreditten mellem skattekonti i stedet for at modtage en kontant tilbagebetaling.

Coretax, e-Faktur og e-Bupot: Hvad ejere af PT PMA-virksomheder bør vide

Hvis det er et stykke tid siden, du har haft med den indonesiske skatteforvaltning at gøre, har forholdene ændret sig markant. Coretax er DJP’s integrerede skatteforvaltningssystem. Det samler de vigtigste skatteprocesser på én platform, herunder registrering af skatteydere, indsendelse af selvangivelser (SPT), skattebetaling, administration af skatteyderkonti, revision og opkrævning. For et PT PMA betyder det, at dit NPWP, direktøradgang, Kode Otorisasi DJP, skatteroller, PKP-status, betalingshistorik og indberetningsoplysninger skal kontrolleres regelmæssigt, inden indberetningen af selvangivelsen påbegyndes.

Tænk på funktionen »Taxpayer Account Management« (TAM) som en kontoudskrift for dine skatter; den viser din skattemæssige situation i realtid for alle skattetyper i ét overblik. DJP har nu et langt bedre overblik over din økonomi end tidligere, og uoverensstemmelser mellem indberetningerne er nemmere at opdage.

Hvad der er ændret i praksis: skatteregistrering, indsendelse af selvangivelser (SPT), betaling, kommunikation i forbindelse med revision og dokumenthåndtering foregår alt sammen via dette system. For en PT PMA betyder det, at dit NPWP, direktøradgang, Kode Otorisasi DJP (KODJP), skatteroller og PKP-status skal verificeres og holdes opdateret i systemet, inden indberetningen påbegyndes.

Det skal du have klar:

- Et gyldigt NPWP-nummer og en verificeret Coretax-konto med et elektronisk certifikat (sertifikat elektronik) for bestyrelsesmedlemmer

- NIB (virksomhedsidentifikationsnummer) fra OSS-RBA

- Selskabsdokumenter og oplysninger om bestyrelsesmedlemmer er bekræftet i systemet

- Lønoplysninger synkroniseret med dine PPh 21-indberetninger

- Leverandørfakturaer og kontrakter til dokumentation for kildeskat i henhold til PPh 23

- Adgang til e-Faktur og NSFP (skattefakturanummerrække), hvis du er en PKP

- Regnskaber og regnskabsmæssig afstemning i forbindelse med den årlige indberetning

e-Bupot-systemet bruges til at udarbejde kildeskatteattester, eller »bukti potong«, for relevante kildeskatteforhold. Køberrelateret kildeskat og kildeskat på medarbejderlønninger bør gennemgås omhyggeligt, da de kan følge forskellige indberetningsprocedurer. Under SPT Masa Unifikasi samles flere kildeskatstyper i en enkelt månedlig indberetning, men din revisor bør stadig bekræfte, hvilke skattetyper der er gældende for din PT PMA.

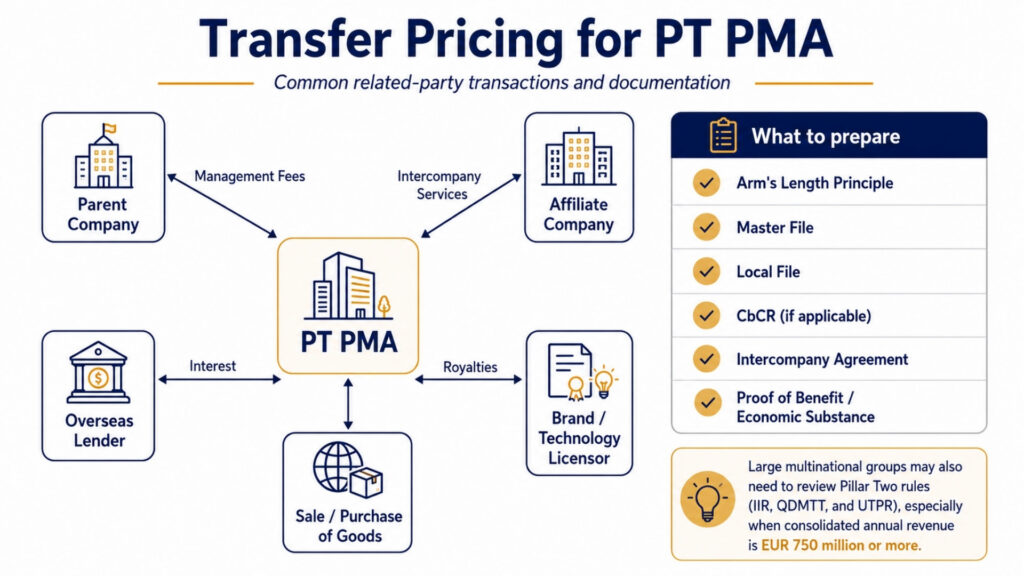

Overførselspriser for PT PMA

Hvis din PT PMA indgår transaktioner med nærtstående parter, moderselskaber, tilknyttede virksomheder eller enheder med fælles aktionærer, finder reglerne om interne priser anvendelse. Indonesien kræver, at disse transaktioner prissættes, som om de blev gennemført mellem uafhængige parter (armlængdeprincippet).

Når der kræves dokumentation for interne priser

I henhold til finansministerens bekendtgørelse nr. 172/2023 skal PT-PMA’er, der har transaktioner med nærtstående parter, der overstiger visse tærskelværdier, udarbejde en hovedfil og lokal fil. Virksomheder i multinationale koncerner, der overskrider en bestemt tærskel for den konsoliderede omsætning, kan også være forpligtet til at udarbejde en land-for-land-rapport (CbCR).

Typiske transaktioner med nærtstående parter, der udløser dette, er: forvaltningshonorarer betalt til et moderselskab, royalties for brug af et varemærke eller en teknologi, renter på aktionærlån, gebyrer for tjenesteydelser mellem selskaber samt køb eller salg af varer til priser, der afviger fra markedsprisen.

Dokumentationen skal ikke blot vise, hvad prisen var, men også hvorfor den var rimelig. “Vores forældre opkrævede dette beløb fra os” er ikke nok. Der skal foreligge en benchmarkanalyse, data om sammenlignelige transaktioner, en koncernintern aftale samt bevis for faktisk økonomisk substans og den modtagne fordel for de tjenesteydelser, der er betalt for.

For store multinationale koncerner er der endnu et aspekt, man skal være opmærksom på: Indonesien har udstedt nationale regler for den globale minimumsbeskatningsramme (søjle 2). Income Inclusion Rule (IIR) og Qualified Domestic Minimum Top-up Tax (QDMTT) træder i kraft fra 2025, mens Undertaxed Profits Rule (UTPR) træder i kraft fra 2026. Dette berører kun store multinationale koncerner med en konsolideret årlig omsætning på 750 millioner euro eller mere, men hvis jeres PT PMA er en del af en sådan koncern, bør jeres transfer pricing og koncerninterne struktur gennemgås i den sammenhæng.

Almindelige fejl i forbindelse med PT- og PMA-beskatning

Ud fra den antagelse, at skatteforpligtelser opstår ved indtægter

Skatteforpligtelser venter ikke på indtægter. Et nyt PT PMA-selskab kan stadig have indberetningspligt, selv før det har tjent en eneste rupiah, især hvad angår den årlige selskabsskatteangivelse og visse månedlige skattetyper, afhængigt af selskabets aktive skatteforpligtelser, som er registreret i Coretax. Tjek, hvilke skattetyper der er aktive hos dit KPP (lokale skattekontor) eller via din Coretax-konto. Mange nyregistrerede PT PMA’er opdager dette på den hårde måde, når de bliver pålagt bøder for forsinket indberetning for perioder, som de antog ikke var omfattet.

Uden at tage højde for den månedlige kildeskat

Selv en enkelt betaling til en leverandør for en ydelse eller en enkelt lønudbetaling medfører en indberetningspligt i henhold til PPh 23 eller PPh 21 i den pågældende måned. Udenlandske investorer, der selv administrerer deres virksomheder, undlader undertiden i flere måneder at indsende månedlige selvangivelser, idet de antager, at der ikke er noget at indberette, fordi de kun har betalt nogle få fakturaer. DJP’s Coretax-system markerer uoverensstemmelser mellem betalingsdata og indberetningshistorikken; en manglende månedlig indberetning er en almindelig udløser for skatterevision som kan medføre, at hele din overholdelseshistorik bliver genstand for en gennemgang.

Anvendelse af traktatsatser uden en gyldig DGT-formular

Dette er et veldokumenteret problem. Et PT PMA-selskab nedsætter sin PPh 26-kildeskat på udbytte, der udbetales til et hollandsk moderselskab, fra 20% til 10% med henvisning til skatteaftalen mellem Indonesien og Holland, men formularen DGT blev ikke indhentet før udbetalingen. DJP kan helt afvise aftalefordelen, hvilket medfører, at de fulde 20% skal betales plus bøder og renter.

Behandling af regnskabsmæssigt overskud som skattepligtigt overskud

Dette volder problemer for økonomiafdelinger uden erfaring med indonesisk skattelovgivning. Nettoresultatet i resultatopgørelsen er et udgangspunkt, ikke det endelige svar. Der skal foretages skattemæssige justeringer, visse udgifter skal lægges til igen, og visse indtægter kan blive justeret. At indsende årsopgørelsen ved direkte at anvende det regnskabsmæssige overskud uden en ordentlig skattemæssig afstemning er en velkendt udløser for skatterevision. Hvis DJP opdager uoverensstemmelsen under en skatterevision, kan de udstede en SKPKB (Surat Ketetapan Pajak Kurang Bayar), en skattebeslutning vedrørende manglende betaling, der fastsætter det manglende skattebeløb samt renter og bøder.

Overskridelse af fristerne for momsfakturaer

e-Faktur-fakturaer skal udstedes senest ved udgangen af den måned, der følger efter transaktionen. Hvis du venter for længe, kan din kunde ikke fratrække indgående moms, hvilket skader jeres forretningsforhold, og du risikerer at blive pålagt bøder. Afvist indgående moms er et af de mest almindelige økonomiske tab ved en skatterevision.

At glemme LKPM, fordi “det ikke har noget med skat at gøre”

Det er rigtigt, at LKPM (Laporan Kegiatan Penanaman Modal, dvs. rapport om investeringsaktiviteter) ikke er en selvangivelse. Den indsendes kvartalsvis via OSS-RBA til BKPM. Men hvis du undlader at indsende den, kan det medføre problemer med din licens, hvilket derefter kan skabe en række problemer for din skatteoverholdelse. I henhold til de seneste regler kan manglende indsendelse nu føre til inddragelse af licensen. Den hører hjemme i samme overholdelseskalender som dine skatteindberetninger.

Tjekliste for overholdelse af skattereglerne for PT PMA-virksomheder

Brug dette hver måned og hvert år for at holde styr på dine forpligtelser:

Månedligt:

- Bekræft, at adgangen til NPWP- og Coretax-kontoen er aktiv

- Udfør lønberegning i henhold til PPh 21 og indsend kildeskatteopgørelsen (e-Bupot)

- Gennemgå alle leverandørbetalinger for at vurdere, om PPh 23 finder anvendelse

- Beregn og betal PPh 25-ratebetalingen

- Kontroller, om der er forpligtelser i henhold til PPh 26 (udlandsbetalinger)

- Indsend momsangivelse, hvis du er registreret som PKP, og udsted alle e-fakturaer til tiden

- Afstemme kontoudtog, lønopgørelser og selvangivelser

Årligt:

- Bekræft, at PKP-status er opdateret

- Udarbejde årsregnskaber (og reviderede regnskaber, hvor dette er lovpligtigt)

- Fuldstændig skatteafstemning (regnskabsmæssigt overskud → skattepligtig indkomst)

- Beregn tillægget til PPh 29, hvis de forudbetalte PPh 25-afdrag ikke dækker den endelige selskabsskat

- Gennemgå risikoen for interne prisfastsættelse i forbindelse med transaktioner med nærtstående parter

- Tjek beskatningen af udbytte og aktionærer

- Indsend årsopgørelsen for selskaber senest den 30. april

- Gem kvitteringer for alle indsendelser og betalinger

Hvornår bør en PT PMA benytte sig af en skatterådgiver?

Du bør seriøst overveje at hyre en autoriseret skatterådgiver i Indonesien (skatterådgiver), hvis et af følgende forhold gør sig gældende:

- Jeres virksomhed har udenlandske aktionærer der modtager udbytte

- Du betaler udenlandske leverandører for ledelses-, IT-, royalty- eller tekniske tjenester

- Du er registreret som en PKP og håndtere et betydeligt momsbeløb

- Du har medarbejdere, både lokale og udstationerede

- Du har transaktioner med nærtstående parter med datterselskaber eller moderselskaber

- Du er ved at forberede dig til din første årlig selskabsskatteangivelse

- Du har modtaget en meddelelse eller en forespørgsel fra KPP (det lokale skattekontor)

En god PT PMA-skatteservice tjener sig selv ind gennem undgåede bøder, korrekt anvendte fradrag og korrekt udnyttede fordele i henhold til skatteaftaler. Omkostningerne ved en fejl, især inden for transfer pricing eller kildeskat i henhold til artikel 26, overstiger næsten altid omkostningerne ved professionel rådgivning.

Ofte stillede spørgsmål om skatteforpligtelser i forbindelse med PT PMA

Hvilke skatter skal en PT PMA betale i Indonesien? Et PT PMA-selskab betaler selskabsskat (PPh Badan), månedlige kildeskatter (PPh 21, PPh 23, PPh 25, PPh 26), moms, hvis det er registreret som PKP, ejendomsskat, hvis det ejer fast ejendom, samt stempelafgift på relevante dokumenter. Der kan også kræves dokumentation for interne priser.

Er selskabsskatten for PT PMA 22%? Ja, den almindelige selskabsskattesats er 22% af den skattepligtige nettoindkomst. Børsnoterede selskaber, der opfylder noteringskravene, kan betale 19%. Små virksomheder med en omsætning på under 50 milliarder IDR kan få en delvis nedsættelse på den del af omsætningen, der ligger under et bestemt beløb.

Skal en PT PMA indsende månedlige skatterapporter? Ja. Der skal indsendes månedlige rapporter for PPh 21 (kildeskat for lønmodtagere), PPh 23 (betalinger for lokale tjenesteydelser), PPh 25 (rater til selskabsskat), PPh 26 (betalinger til udlandet) og moms. Selv hvis der mangler én eneste måned, medfører det manglende overholdelse af reglerne og bøder.

Skal et nyt PT PMA-selskab indgive selvangivelse, selvom det ikke har nogen indtægter? Muligvis ja. En ny PT PMA kan stadig have indberetningsforpligtelser, før virksomheden genererer indtægter, især hvad angår den årlige selskabsskatteangivelse og visse månedlige skatteformer, afhængigt af hvilke skatteforpligtelser der er gældende. Tjek dine gældende skatteforpligtelser via din Coretax-konto eller hos KPP for at undgå uventede bøder for perioder, hvor der ikke er indsendt indberetninger.

Hvornår skal en PT PMA registrere sig som momspligtig? Når den årlige omsætning når op på eller forventes at nå 4,8 milliarder IDR, er det obligatorisk at registrere sig som PKP. Det er også tilladt at registrere sig frivilligt, før denne tærskel nås.

Kan en PT PMA benytte sig af den endelige beskatningsordning 0.5%? Ikke automatisk. Nogle selskabsskattepligtige med en bruttoomsætning på op til 4,8 milliarder IDR kan være berettiget til 0,5%-ordningen for endelig indkomstskat, men berettigelsen afgøres fra sag til sag og er tidsbegrænset. Det afhænger af virksomhedens skattepligtige status, forretningsaktivitet, registreringsdato og valg af skattebehandling. Et PT PMA-selskab bør ikke gå ud fra, at det er berettiget, uden først at have fået dette bekræftet af en skatterådgiver.

Er udbytte til udenlandske aktionærer skattepligtigt? Ja. Udbytte, der udbetales til en udenlandsk aktionær, er omfattet af PPh 26 med en standardskattesats på 20%. Der kan gælde en lavere sats i henhold til en skatteaftale, hvis den udenlandske part indsender en gyldig DGT-formular.

Hvad sker der, hvis en PT PMA indsender sin selvangivelse for sent? Forsinket indsendelse medfører administrative bøder: 100.000 IDR for de fleste månedlige selvangivelser, 500.000 IDR for en forsinket momsangivelse og 1.000.000 IDR for en forsinket årlig selskabsskatteangivelse. For for lidt betalt skat pålægges der desuden rentestraf baseret på den gældende månedlige rentesats fra Finansministeriet (MoF) plus et tillæg i op til 24 måneder. Gentagne forsinkelser i indsendelsen øger risikoen for revision og kan udløse et skatteansættelsesbrev (SKPKB) eller en skatteopkrævning (Surat Tagihan Pajak, STP).

Hvad er forskellen mellem LKPM og skatterapportering? LKPM er en rapport om investeringsaktiviteter, der indsendes til BKPM via OSS-RBA. Den følger op på fremskridtene i forhold til din investeringsplan og er ikke en selvangivelse. Skatteindberetningen indsendes til DJP via Coretax. Begge er obligatoriske for PT PMA’er, og begge har hver deres frister og konsekvenser ved manglende overholdelse.

Skal alle PT PMA’er have dokumentation for interne priser? Det gælder ikke alle PT PMA’er, men enhver PT PMA, der indgår transaktioner med nærtstående parter, tilknyttede selskaber, moderselskaber eller enheder med fælles aktionærer, skal vurdere, om der kræves dokumentation i henhold til PMK 172/2023. Tærskelværdierne og dokumentationstyperne afhænger af transaktionsomfanget og koncernens størrelse.

Klar til at ansøge eller forlænge dit visum?

Lad vores visumspecialister håndtere din ansøgning.