Tax Obligations for PT PMA in Indonesia 2026

If you’ve just set up a PT PMA, or you’re planning to, this guide is written for you. Whether you’re a foreign investor, a director of a foreign-owned company, or someone on the finance team trying to figure out what Indonesia’s tax system actually wants from you, you’re in the right place.

Here’s the short answer you need right now: a PT PMA must handle corporate income tax, a set of monthly withholding taxes, VAT if you’re registered as a PKP (taxable entrepreneur), an annual tax filing, and sometimes transfer pricing documentation. That’s the core of it.

But the details matter, and getting them wrong costs real money. Tax rules in Indonesia change regularly, so always confirm your specific situation with a licensed tax consultant or registered tax firm.

Indice dei contenuti

Quick Summary: What Taxes Does a PT PMA Need to Pay?

| Obligation | When It Applies | Filing Frequency |

| Corporate Income Tax / PPh Badan | The company earns a taxable profit | Annuale |

| PPh 25 | Monthly CIT installment payments | Monthly |

| PPh 29 | Annual CIT top-up when installments fall short of the final liability | Annual (before SPT filing) |

| PPh 21 | The company has employees | Monthly |

| PPh 23 | Payments to local vendors for services, rent, royalties | Monthly |

| PPh 26 | Payments to foreign parties | Monthly |

| VAT / PPN | The company is registered as PKP | Monthly |

| PBB (Land and Building Tax) | The company owns or uses taxable land/building | Annual or by notice |

| Bea Meterai (Stamp Duty) | Certain official documents and contracts | Per document |

| Transfer pricing documentation | Related-party transactions | Annual or upon request |

Is a PT PMA Taxed Differently from a Local PT?

Same basic tax duties as local companies

Here’s something many foreign investors don’t realize until they’re already knee-deep in paperwork: a PT PMA is a fully Indonesian legal entity. That means it generally follows the same Indonesian corporate tax rules as any local PT (limited liability company). Indonesia uses a self-assessment system; your company is responsible for calculating, paying, and reporting its own tax liabilities each period.

The DJP, the Directorate General of Taxes, treats your foreign-owned company the same way it treats a domestically owned one in terms of core reporting structure. That said, the DJP can still issue a tax assessment letter (SKPKB or Surat Ketetapan Pajak Kurang Bayar) after a tax audit, or a tax collection notice (Surat Tagihan Pajak / STP) if filings are missed or tax is underpaid.

But there are extra layers that foreign-owned companies face

That “same rules” principle only goes so far. A PT PMA often has complications that a purely local PT doesn’t deal with:

- Foreign shareholder dividends, payments back to a parent company or overseas investor, trigger Article 26 withholding tax

- Cross-border service fees, if you pay a foreign company for management, IT, or technical services, which trigger withholding obligations

- Tax treaty use, if a treaty exists between Indonesia and your shareholder’s country, you may qualify for a reduced rate, but only with the right paperwork (Form DGT)

- Transfer pricing, transactions between your PT PMA and related parties overseas, need to be at arm’s length and documented

- Permanent establishment risk, if your foreign parent is too involved in operations, they could be deemed a BUT (permanent establishment) in Indonesia

Think of it this way: the tax foundation is the same, but there’s an extra floor built on top specifically for companies with foreign connections.

Corporate Income Tax for PT PMA

The standard CIT rate

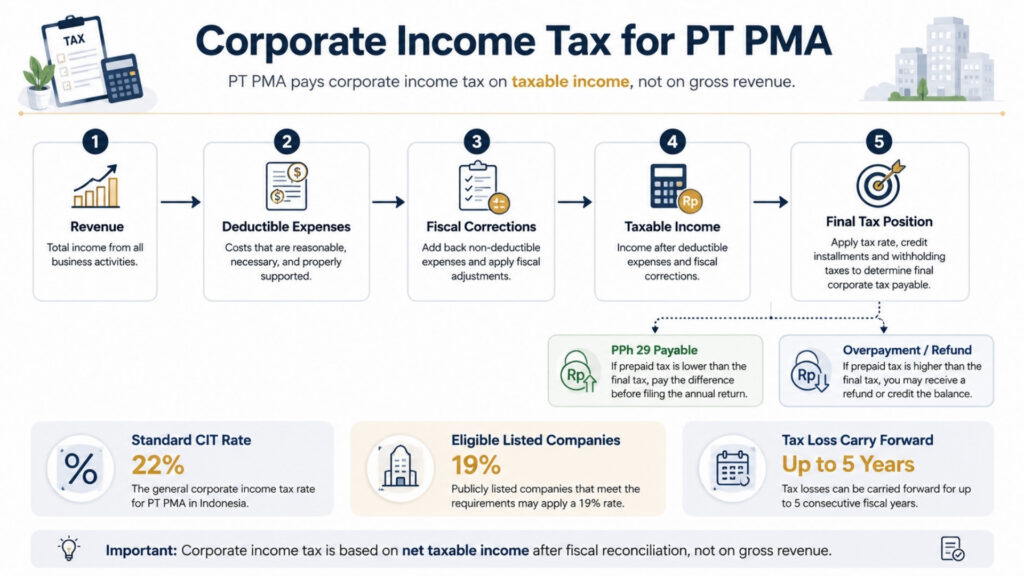

Indonesia’s standard corporate income tax rate is 22% on net taxable income, not on gross revenue, which is an important distinction. You only pay CIT on what’s left after deducting allowable business expenses from your income.

If your PT PMA is a public company that meets the minimum stock exchange listing requirements, you may qualify for a 3% rate reduction, bringing your effective CIT rate down to 19%.

How taxable income is actually calculated

This is where many foreign investors get tripped up. Your accounting profit and your fiscal profit are not the same thing.

Here’s a simple way to think about it: your accountant prepares financial statements following commercial accounting standards. Indonesian tax law also follows the accrual principle; income is recognized when it is earned, and expenses are recognized when they are incurred, regardless of when cash actually moves.

But the DJP has its own rules about what expenses are deductible and what aren’t. That difference between commercial accounting and fiscal treatment is resolved through a fiscal reconciliation (rekonsiliasi fiskal), which you must complete every year before you can file your annual tax return.

Common non-deductible expenses include entertainment costs without proper documentation, certain fines and penalties, and personal expenses that got mixed into company books, something that happens more often than anyone likes to admit. Tax losses can be carried forward for up to five years under standard rules.

Small company tax relief and the 0.5% final tax regime

Two important notes here. First, small companies with annual turnover not exceeding IDR 50 billion may receive a 50% discount on CIT, but only on the taxable income portion tied to turnover up to IDR 4.8 billion.

Second, a PT PMA should not assume it can use the 0.5% final income tax regime just because its turnover is still below IDR 4.8 billion. Some corporate taxpayers with gross turnover up to IDR 4.8 billion may fall under this regime, but eligibility is case-specific and time-limited. The company’s taxpayer status, business activity, registration date, and choice of tax treatment can all affect the result. Always confirm this with a tax consultant before using the 0.5% rate in any tax calculation.

Annual corporate tax return deadline

The annual corporate income tax return, called SPT Tahunan Badan, is due no later than four months after the end of your fiscal year. For companies using the calendar year (January to December), that deadline is 30 aprile. To file, you’ll need your financial statements (and audited statements where legally required), your fiscal reconciliation, and records of all advance tax payments made during the year.

Monthly Tax Obligations for PT PMA

This is where most of the ongoing work sits. Think of monthly tax obligations like a subscription you can’t cancel; they run every single month, whether you have revenue or not.

PPh 21 for employees

If your PT PMA has employees, local or expatriate, you’re required to withhold income tax from their salaries each month and report it. This is PPh 21. The monthly return for employee and foreign individual withholding is the SPT Masa PPh 21/26, filed each month through Coretax.

You’ll need employee NPWP numbers (or NIK for those without an NPWP), payroll records that align with your BPJS social security contributions, and consistent reporting through Coretax. Under PMK-168/2023, the monthly withholding calculation now uses an effective rate (TER) method rather than the old net income estimation approach.

PPh 23 for local service payments

Every time your PT PMA pays a local vendor for services, royalties, or the rental of non-land/building assets such as equipment or vehicles, you may need to withhold PPh 23 from the payment. Land and building rental is usually treated separately under Article 4(2) Final Income Tax, so do not group office rent into PPh 23 without checking the tax object first.

PPh 23 withholding for local service payments is consolidated with other withholding taxes into the SPT Masa Unifikasi, the unified monthly withholding tax return filed through Coretax. Check your vendor’s tax status; some are exempt, some have different rates. Missing this obligation is one of the most common compliance gaps for new PT PMAs.

PPh 25 monthly CIT installments

If your total prepaid tax is lower than your final annual corporate income tax due, the remaining shortfall is commonly handled as PPh 29, or underpaid annual corporate income tax. This amount must be paid before filing the annual corporate tax return. This is why monthly PPh 25 installments, withholding tax credits, and year-end fiscal reconciliation should be checked together before submission.

Conversely, if your PPh 25 installments exceed your actual annual tax liability, you end up in an overpayment position on your CIT return. That overpayment can be offset against other tax liabilities through a pemindahbukuan (tax book transfer) or claimed back through a formal tax refund request to the DJP. Either path requires supporting documentation, so keep your payment records and installment calculations organized throughout the year.

PPh 26 for payments to foreign parties

This is where PT PMA compliance gets more complex than local companies. When your company pays dividends to a foreign shareholder, interest on a loan from an overseas lender, royalties to a foreign brand owner, or management fees to a parent company, you need to withhold PPh 26 at a default rate of 20%.

However, and this is important, if a double tax treaty (DTA) exists between Indonesia and the recipient’s country, you may qualify for a reduced treaty rate. But you can’t just apply the lower rate on your own.

For passive income like dividends, interest, and royalties, the foreign recipient must be the beneficial owner of that income and must provide a certified Certificate of Domicile (CoD), submitted as Form DGT to the DJP. Without a valid CoD/Form DGT accepted by the DJP, the 20% default rate applies, no exceptions. The concept of beneficial ownership matters: if the foreign party is a conduit or holding structure rather than the true economic owner, the treaty benefit can be denied even if Form DGT is submitted.

VAT / PPN Obligations for PT PMA

When a PT PMA must register as PKP

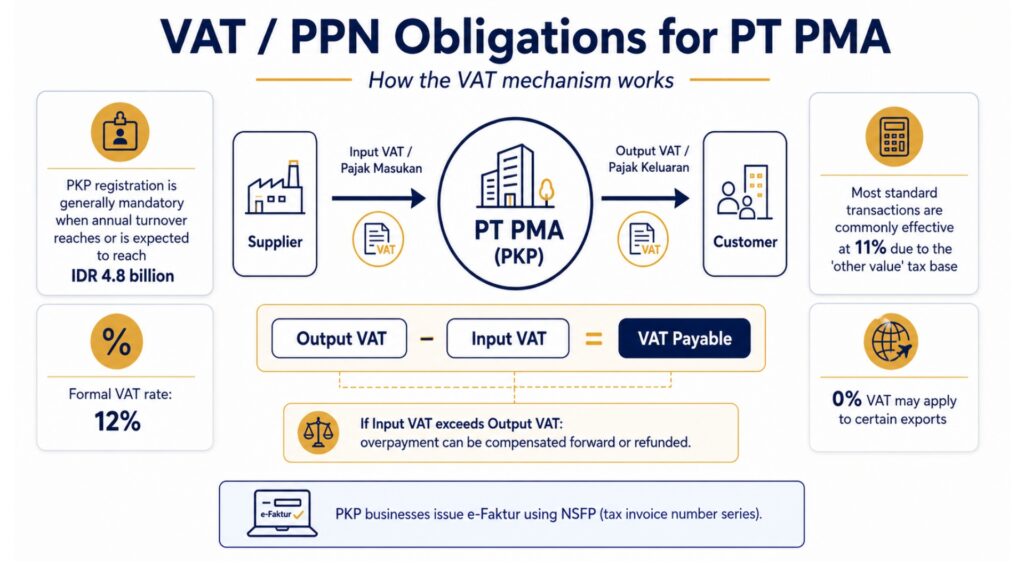

Once your PT PMA’s annual turnover hits or is expected to hit IDR 4.8 billion, you’re required to register as a PKP, a Pengusaha Kena Pajak, or taxable entrepreneur. After registration, you collect VAT on your sales and can claim back VAT you’ve paid on business purchases. Companies in early-stage operations can also register voluntarily before hitting that threshold if it makes business sense.

The current VAT rate in Indonesia

Here’s where even experienced finance professionals get confused. Indonesia’s formal VAT rate is 12%. But most goods and services are still effectively taxed at 11% due to a mechanism called the DPP Nilai Lain (other value tax base), a deemed tax base that applies to most standard transactions in place of the full transaction value. The 12% effective rate only kicks in for certain luxury goods. Exports of goods and some services are zero-rated. When you’re building financial models or pricing your services, use 11% as your working assumption for most standard B2B transactions, but confirm with your tax advisor for your specific business type.

VAT invoices, input VAT, and common mistakes

Once you’re a PKP, you must issue tax invoices, called e-Faktur, for every taxable sale. These must be issued through the DJP’s e-Faktur system using an NSFP (Nomor Seri Faktur Pajak, or tax invoice number series) allocated by the DJP. Pajak Keluaran (output VAT), what you collect from customers, minus Pajak Masukan (input VAT), what you paid to your PKP vendors, equals what you remit to the government each month.

If input VAT exceeds output VAT in a given period, you have a VAT overpayment position. That overpayment can be carried forward to the next period or claimed back through a formal tax refund request, which, if approved, results in the DJP issuing an SKPLB (Surat Ketetapan Pajak Lebih Bayar), the official overpayment assessment that authorizes the refund.

The most painful VAT mistake? Missing the invoice issuance deadline. Input VAT credits can be rejected if the invoice wasn’t issued on time or doesn’t meet the technical requirements. One missing field in an e-Faktur can disqualify a credit worth millions of rupiah.

Other Taxes and Compliance Items

Article 4(2) Final Income Tax covers certain transactions taxed on a final basis, land and building rental income, construction services, and a few other items. The rates vary by category, and these taxes are final, meaning you can’t deduct the base income again in your annual return.

PBB (Land and Building Tax) is now administered as a regional tax under PBB-P2 rules, with a maximum rate of 0.5% depending on regional government regulations. Taxable value is based on the NJOP (Nilai Jual Objek Pajak, or assessed sale value). It’s worth noting that PBB sectoral rules apply to certain industries, including mining, oil and gas, plantation, and forestry operations, which are governed by separate central government PBB provisions rather than the regional PBB-P2 framework.

If your PT PMA operates in any of these sectors, the applicable PBB rules, rates, and filing channels differ from the standard regional tax process. If your PT PMA transfers land or building rights, BPHTB (Land and Building Rights Transfer Tax) may also apply at a maximum rate of 5% on the transaction value above a threshold.

Bea Meterai (Stamp Duty) of IDR 10,000 applies to contracts, agreements, and certain official documents above specified values. Easy to forget, surprisingly important during audits and legal disputes.

Local/regional taxes (PBJT) apply in certain industries, hotels, restaurants, entertainment venues, and local service businesses may owe additional taxes to regional governments under the Regional Tax and Retribution Law. This is separate from national tax obligations and can catch hospitality-focused PT PMAs off guard.

PPh 22, Import VAT, and Customs Duties

If your PT PMA imports goods into Indonesia, tax compliance goes beyond corporate income tax and VAT. Import transactions can involve import duty (Bea Masuk), import VAT (PPN impor), PPnBM (Luxury Goods Sales Tax) on certain luxury items, and Article 22 Income Tax (PPh 22). These amounts are usually handled during customs clearance, but they still affect your tax records and annual fiscal reconciliation.

This matters especially for PT PMAs in trading, manufacturing, construction, hospitality, and retail. Keep customs documents, import declarations, tax payment slips (billing codes), commercial invoices from overseas suppliers, and supplier contracts organized together. A commercial invoice is the primary document used by customs to assess the dutiable value, and your accountant will also need it to reconcile import costs, input VAT (Pajak Masukan), inventory value, and prepaid income tax at year-end. Missing or inconsistent commercial invoices can create discrepancies between customs records and tax filings, a common tax audit trigger.

PT PMA Tax Filing Deadlines

| Tax Return | Filing Deadline |

| Annual Corporate Tax Return (SPT Tahunan Badan) | 4 months after tax year-end (April 30 for calendar-year companies) |

| PPh 21 / 26 (employee / foreign withholding) | 20th of the following month |

| PPh 23 / 26 (service / foreign withholding) | 20th of the following month |

| PPh 25 (monthly CIT installment) | 20th of the following month |

| Article 4(2) Final Income Tax | 20th of the following month |

| VAT / PPnBM | End of the following month |

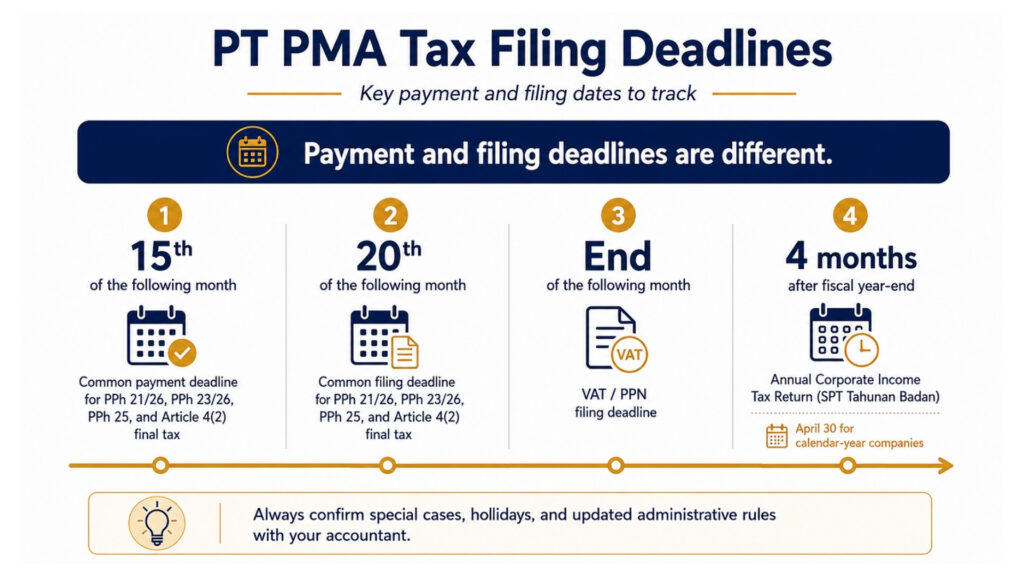

Payment and filing deadlines are not the same; this is a practical gap that trips up many PT PMAs. Here’s a clearer breakdown:

| Tipo di imposta | Payment Deadline | Filing Deadline |

| PPh 21 / 26 | Generally, by the 15th of the following month | By the 20th of the following month |

| PPh 23 / 26 | Generally, by the 15th of the following month | By the 20th of the following month |

| PPh 25 | Generally, by the 15th of the following month | By the 20th of the following month |

| Article 4(2) Final Tax | Generally, by the 15th of the following month | By the 20th of the following month |

| VAT / PPN | Before filing the VAT return | End of the following month |

| Annual CIT / SPT Tahunan Badan | Before filing the annual return | 4 months after the fiscal year-end |

Late payment carries interest penalties calculated based on the applicable monthly Ministry of Finance (MoF) interest rate plus a surcharge, for up to 24 months. Late filing also carries separate administrative fines: IDR 100,000 for most monthly returns, IDR 500,000 for a late VAT return, and IDR 1,000,000 for a late annual CIT return. Confirm current rates with your accountant, as the MoF interest rate is set periodically.

One practical note on how payments work: tax payments in Indonesia are made through a bank persepsi, a government-appointed bank or payment channel authorized to receive tax deposits on behalf of the DJP.

Payments are made by generating a billing code (Kode Billing) in Coretax and settling it via a bank persepsi or an approved e-payment channel. If your PT PMA has an overpayment on one tax type that you want to apply against a liability on another, that is done through pemindahbukuan (a tax book transfer), a formal request to the DJP to move the credit across tax accounts rather than receiving a cash refund.

Coretax, e-Faktur, and e-Bupot: What PT PMA Owners Should Know

If you haven’t dealt with Indonesian tax administration in a while, the landscape has changed significantly. Coretax is DJP’s integrated tax administration system. It brings key tax processes into one platform, including taxpayer registration, SPT filing, tax payment, Taxpayer Account Management, audit, and collection. For a PT PMA, this means your NPWP, director access, Kode Otorisasi DJP, tax roles, PKP status, payment history, and filing records need to be checked regularly before tax filing begins.

Think of the Taxpayer Account Management (TAM) feature like a bank statement for your taxes; it shows your real-time tax position across all tax types in one view. The DJP now has much tighter visibility into your financials than before, and inconsistencies between filings are easier to flag.

What’s changed in practice: tax registration, SPT filing, payment, audit communication, and document flow all run through this system. For a PT PMA, this means your NPWP, director access, Kode Otorisasi DJP (KODJP), tax roles, and PKP status need to be verified and kept current in the system before filing begins.

What you need to have ready:

- Active NPWP and verified Coretax account with sertifikat elektronik (electronic certificate) for directors

- NIB (Business Identification Number) from OSS-RBA

- Company deed and director data confirmed in the system

- Payroll records synchronized with your PPh 21 filings

- Vendor invoices and contracts to support PPh 23 withholding

- e-Faktur access and NSFP (tax invoice number series) if you’re a PKP

- Financial statements and fiscal reconciliation for annual filing

The e-Bupot system is used to generate withholding tax slips, or bukti potong, for relevant withholding tax transactions. Vendor-related withholding taxes and employee salary withholding should be reviewed carefully because they may use different reporting flows. Under SPT Masa Unifikasi, several withholding tax types are consolidated into a single monthly filing, but your accountant should still confirm which tax types are active for your PT PMA.

Transfer Pricing for PT PMA

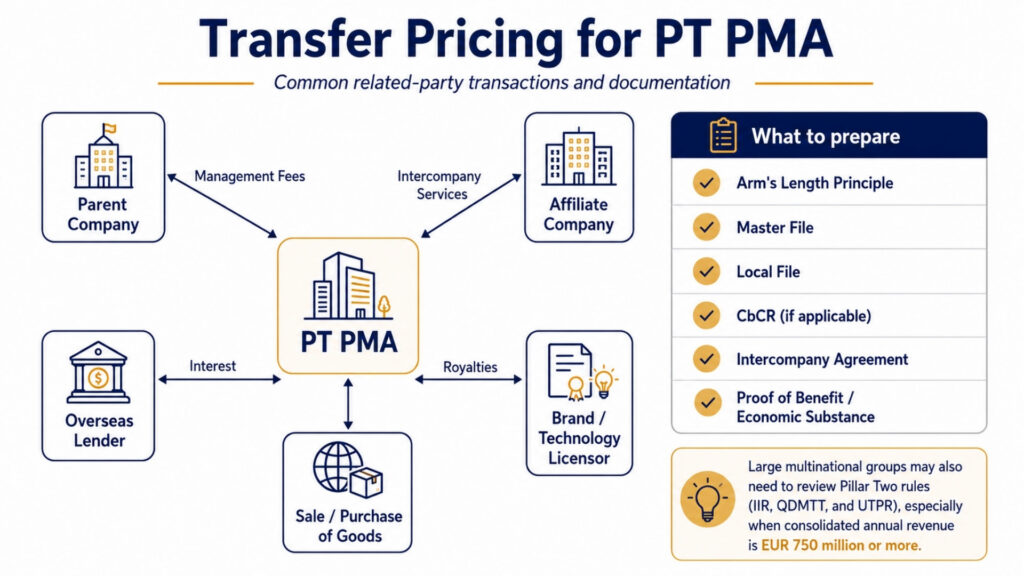

If your PT PMA has transactions with related parties, parent companies, affiliated businesses, or entities with common shareholders, transfer pricing rules apply. Indonesia requires that these transactions be priced as if they were done between unrelated parties (the arm’s-length principle).

When transfer pricing documentation is required

Under Minister of Finance Regulation No. 172/2023, PT PMAs with related-party transactions above certain thresholds must prepare a master file e local file. Companies in multinational groups above a specific consolidated revenue threshold may also need a Country-by-Country Report (CbCR).

Common related-party transactions that trigger this: management fees paid to a parent company, royalties for using a brand or technology, interest on shareholder loans, intercompany service fees, and purchases or sales of goods at non-market prices.

The documentation must show not just what the price was, but why it was fair. “Our parents charged us this” is not enough. You need a benchmark analysis, comparable transaction data, an intercompany agreement, and proof of actual economic substance and benefit received for any services paid for.

For large multinational groups, there is one more layer to be aware of: Indonesia has issued domestic rules for the global minimum tax framework (Pillar Two). The Income Inclusion Rule (IIR) and Qualified Domestic Minimum Top-up Tax (QDMTT) apply from 2025, with the Undertaxed Profits Rule (UTPR) from 2026. This only affects large multinational enterprise groups with consolidated annual revenue of EUR 750 million or more, but if your PT PMA is part of such a group, your transfer pricing and intercompany structure should be reviewed in that context.

Common PT PMA Tax Mistakes

Assuming tax obligations start with revenue

Tax obligations don’t wait for revenue. A new PT PMA may still have filing duties before earning a single rupiah, especially the annual CIT return and certain monthly tax types, depending on the company’s active tax obligations registered in Coretax. Confirm which tax types are active at your KPP (local tax office) or through your Coretax account. Many newly registered PT PMAs discover this the hard way when they get hit with late filing penalties for periods they assumed didn’t apply.

Ignoring the monthly withholding tax

Even one vendor payment for a service, or one salary payment, creates a PPh 23 or PPh 21 reporting obligation that month. Foreign investors who self-manage their companies sometimes go months without filing monthly returns, assuming there’s nothing to report because they paid only a few invoices. The DJP’s Coretax system flags gaps between payment data and filing history; a missing monthly return is a common tax audit trigger that can pull your entire compliance record into review.

Applying treaty rates without a valid Form DGT

This is a well-documented problem. A PT PMA reduces its PPh 26 withholding on dividends paid to a Dutch parent from 20% to 10%, citing the Indonesia-Netherlands tax treaty, but the Form DGT wasn’t obtained before payment. The DJP can disallow the treaty benefit entirely, making the full 20% due plus penalties and interest.

Treating accounting profit as taxable profit

This trips up finance teams without Indonesian tax experience. Your net profit on the P&L is a starting point, not the final answer. Fiscal corrections must be applied, some expenses must be added back, and some income may be adjusted. Filing your annual return using accounting profit directly, without a proper fiscal reconciliation, is a known tax audit trigger. If the DJP identifies the discrepancy during a tax audit, they can issue an SKPKB (Surat Ketetapan Pajak Kurang Bayar), an underpayment tax assessment, that locks in the tax shortfall plus interest and penalties.

Missing VAT invoice deadlines

e-Faktur invoices must be issued by the end of the month following the transaction. Waiting too long means your customer can’t claim input VAT, which damages your business relationship, and you could face penalties. Rejected input VAT is one of the most common financial hits in a tax audit.

Forgetting LKPM because “it’s not a tax thing”

True, LKPM (Laporan Kegiatan Penanaman Modal, or Investment Activity Report) is not a tax return. It’s filed through OSS-RBA to BKPM quarterly. But skipping it can result in license issues, which then create cascading problems for your tax compliance. As of recent regulations, non-submission can now lead to license revocation. It belongs in the same compliance calendar as your tax filings.

PT PMA Tax Compliance Checklist

Use this every month and every year to stay on top of your obligations:

Monthly:

- Confirm NPWP and Coretax account access is active

- Run PPh 21 payroll calculation and file withholding slip (e-Bupot)

- Review all vendor payments for PPh 23 applicability

- Calculate and pay the PPh 25 installment

- Check for any PPh 26 obligations (foreign payments)

- File VAT return if registered as PKP and issue all e-Faktur on time

- Reconcile bank statements, payroll records, and tax filings

Annually:

- Confirm PKP status is current

- Prepare financial statements (and audited statements where legally required)

- Complete fiscal reconciliation (accounting profit → taxable income)

- Calculate PPh 29 top-up if PPh 25 installments fall short of final CIT liability

- Review transfer pricing exposure for related-party transactions

- Check dividend and shareholder tax treatment

- Submit SPT Tahunan Badan by April 30

- Keep proof of all filing and payment confirmations

When Should a PT PMA Use a Tax Consultant?

You should seriously consider engaging a licensed tax consultant in Indonesia (konsultan pajak) if any of the following apply:

- Your company has azionisti stranieri who receive dividends

- You pay overseas vendors for management, IT, royalty, or technical services

- You are registered as a PKP and deal with a significant VAT volume

- You have employees, local or expatriate

- Hai related-party transactions with affiliates or parent companies

- You’re preparing for your first annual corporate tax return

- You’ve received any notice or query from the KPP (local tax office)

A good PT PMA tax service pays for itself in avoided penalties, correctly claimed deductions, and treaty benefits properly applied. The cost of a mistake, especially on transfer pricing or Article 26 withholding, almost always exceeds the cost of professional advice.

FAQs About PT PMA Tax Obligations

What taxes does a PT PMA pay in Indonesia? A PT PMA pays corporate income tax (PPh Badan), monthly withholding taxes (PPh 21, PPh 23, PPh 25, PPh 26), VAT if registered as a PKP, land and building tax if it holds property, and stamp duty on qualifying documents. Transfer pricing documentation may also be required.

Is PT PMA corporate tax 22%? Yes, the standard corporate income tax rate is 22% on net taxable income. Public companies meeting listing criteria may pay 19%. Small companies with a turnover under IDR 50 billion may get a partial discount on the lower-revenue portion.

Does a PT PMA need to file monthly tax reports? Yes. Monthly reports are required for PPh 21 (employee withholding), PPh 23 (local service payments), PPh 25 (CIT installments), PPh 26 (foreign payments), and VAT. Missing even one month creates compliance gaps and penalties.

Does a new PT PMA need to file taxes if it has no revenue? Possibly yes. A new PT PMA may still have filing duties before generating revenue, especially for the annual CIT return and certain monthly tax types, depending on which tax obligations are active. Confirm your active tax obligations through your Coretax account or with the KPP to avoid unexpected penalties for unfiled periods.

When must a PT PMA register for VAT? When annual turnover reaches or is expected to reach IDR 4.8 billion, PKP registration is mandatory. Voluntary registration before that threshold is also permitted.

Can a PT PMA use the 0.5% final tax regime? Not automatically. Some corporate taxpayers with gross turnover up to IDR 4.8 billion may be eligible for the 0.5% final income tax regime, but eligibility is case-specific and time-limited. It depends on the company’s taxpayer status, business activity, registration date, and tax treatment choice. A PT PMA should not assume it qualifies without first confirming with a tax consultant.

Are dividends to foreign shareholders taxable? Yes. Dividends paid to a foreign shareholder are subject to PPh 26 at a default rate of 20%. A lower rate may apply under a tax treaty if the foreign party submits a valid Form DGT.

What happens if a PT PMA files taxes late? Late filing carries administrative fines: IDR 100,000 for most monthly returns, IDR 500,000 for a late VAT return, and IDR 1,000,000 for a late annual CIT return. Underpaid tax also carries interest penalties based on the applicable monthly Ministry of Finance (MoF) interest rate plus a surcharge, for up to 24 months. Repeated late filings increase audit risk and can trigger a tax assessment letter (SKPKB) or Surat Tagihan Pajak (STP).

What is the difference between LKPM and tax reporting? LKPM is an investment activity report filed with BKPM through OSS-RBA. It tracks your progress against your investment plan and is not a tax return. Tax reporting is filed with the DJP through Coretax. Both are mandatory for PT PMAs, and both have separate deadlines and consequences for non-compliance.

Does every PT PMA need transfer pricing documentation? Not every PT PMA, but any PT PMA that has transactions with related parties, affiliated companies, parent companies, or entities with common shareholders, needs to assess whether documentation is required under PMK 172/2023. The thresholds and documentation types depend on transaction volume and group size.

Sei pronto a richiedere o prolungare il tuo visto?

Lascia che siano i nostri specialisti a gestire la tua domanda di visto.